Buying an apartment complex is more involved than investing in single-family properties and involves a deeper understanding of the financial and management aspects. Typically, you can learn how to buy an apartment complex in seven steps. These steps include deciding if an apartment building is right for you and what type of apartment complex to purchase.

Buying an apartment complex can be broken down into the following seven steps:

1. Decide if Buying an Apartment Complex Is Right for You

Before you start investing in apartment buildings, you want to make sure it’s the right investment strategy for you. Compared to purchasing single-family homes and small multifamily properties, an apartment building requires more research, more time, and oftentimes more capital and additional expenses. It’s important to weigh the pros and cons before buying apartment complexes.

Pros of Buying Apartment Complexes

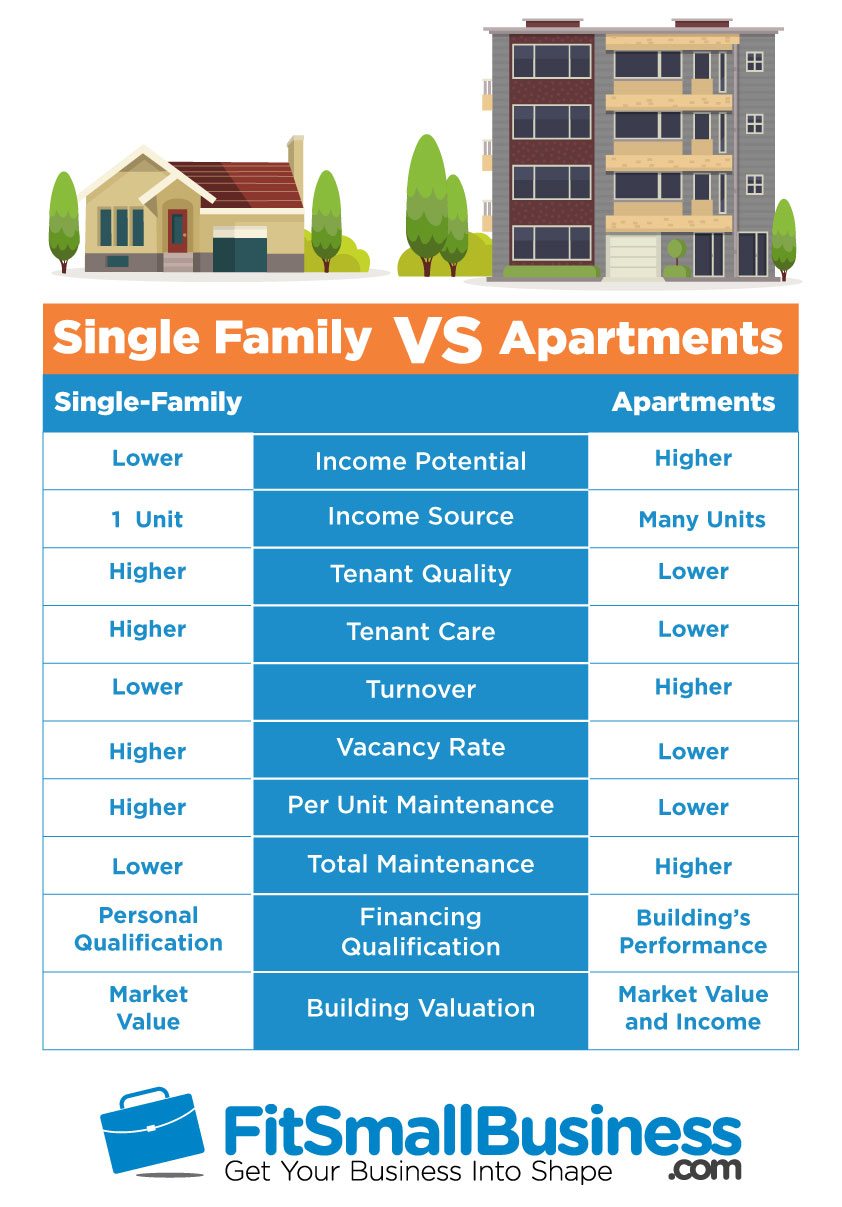

There are many benefits to owning an apartment building. These include recurring income, diversifying the income across many units, lower per-unit maintenance costs, the possibility of extra sources of income over and above the rents, financing based more on the property’s financials than your own, and the building’s value is often a function of rents.

Recurring Income from Buying an Apartment Complex

One of the main reasons for buying apartment buildings is ongoing income. If the deal is right, and the finances are sound, a good apartment building will throw off recurring monthly income, also known as positive cash flow.

Diversifying Income Across Many Units Once Buying an Apartment Complex

If you’re a buy-and-hold investor who typically buys single-family properties, you’re probably familiar with a common vacancy problem. If your property goes vacant, you lose 100 percent of your rent. On the other hand, apartment buildings mitigate the effects of a high vacancy rate. If one unit goes vacant, you still have the others to generate rent to cover expenses and perhaps still generate positive cash flow.

Lower Per-Unit Maintenance Costs of an Apartment Complex

Economies of scale work in the favor of the apartment building owner. For example, if you have to redo a roof, it’s not just for one unit. That repair serves all the units in the building. If you need to repaint, you can use the same paint for multiple units and not have wasted materials resulting from only one unit’s need.

Extra Sources of Income When Buying Apartment Complexes

The larger the building, the more likely you can add additional sources of income, such as vending machines, ATMs and coin-operated laundry facilities. Renting parking spaces and space for billboard advertising can also provide additional income. One pro tip is to charge additional monthly rent for air conditioning units, upgraded appliances, and upgraded kitchens and bathrooms.

Financing Is Based More on the Apartment Complex’s Financials Than Your Own

Unlike a single-family property, financing for apartment buildings is based mainly on the financial performance of the building as opposed to your personal financial and credit situation. So, banks will look mainly at the financial situation with the building for approving a loan. This is advantageous if your FICO score is low.

Apartment Building’s Value Is Often a Function of Rents

When buying apartment buildings, the value of the investment is determined in great part by the financial performance of the building. So, if you can increase the rents, you can increase the value of your holding.

Cons of Buying Apartment Complexes

Buying an apartment complex is more complex than acquiring a single-family home or even a small multi-unit property. The management will be a bit more intensive and the nature of tenants will be different. In addition, expect maintenance to be more of a regular issue and property management to be more expensive.

Buying an Apartment Complex Requires Intensive Management

Once buildings are larger than four units, management becomes a much more intensive process. The ability to manage the property yourself becomes an issue, and you need to consider some form of outside management.

One option is hiring a professional property management company. In other cases, you’ll hire an onsite manager. Both of these come with additional costs and the need to supervise the manager. Typically, property managers charge 10 percent to 20 percent of gross monthly rents.

Tenant Turnover Is Prevalent When Buying an Apartment Complex

When tenants move into a single-family dwelling, it tends to be more for the long-haul. They get to know the neighborhood, their kids go to local schools, etc. Tenants in apartments, on the other hand, are much more transient.

In a single-family home, it’s not uncommon for a tenant to stay five years or more. In an apartment, you’re lucky if a tenant stays more than one year. So, you have to expect tenant turnover, and you will constantly be in the mode of marketing for, and renting to, new occupants.

Less Tenant Care of an Apartment Complex

Even a renter in a single-family dwelling will tend to treat the property like their own home. An apartment, on the other hand, is a different animal. Tenants often don’t tend to treat apartments with the same care. So, damage and maintenance needs beyond the normal wear and tear will be much more prevalent with apartments.

Buying an Apartment Complex Involves High Maintenance Costs

When buying apartment buildings, be prepared for turnover and general lack of care tenants give to their units. You’ll also have more ongoing maintenance with apartments than with single-family units. On a per-unit basis, maintenance costs will be lower the more units a building has (particularly when compared to a single-family dwelling).

However, the overall cost of maintenance will be higher in an apartment building, even with similar square footage to a home. Over at Avail, CEO Ryan Coon cautions investors that when major problems arise, such as a boiler break causing loss of heat to the entire building, they impact more tenants and are more expensive to fix. Replacing the plumbing system for one bathroom, or even for an entire house, is much cheaper than replacing the plumbing for a five-story building.

2. Choose the Type of Apartment Complex to Buy

If you’ve decided that buying an apartment complex is a good option for you, the next step is to consider the type of apartment building you want to acquire. This involves examining your personal and financial criteria for the purchase, the number of units desired, and understanding the class of apartments available for purchase.

More items to consider when choosing the type of apartment complex to buy are:

Examine Your Personal and Financial Criteria Before Investing in an Apartment Complex

Consider your level of ambition and risk threshold, since both will affect the kind of apartment investments you’ll consider. The two main considerations along those lines are the number of units and the return on investment (ROI) you’re seeking.

Consider the Number of Units in the Apartment Complex

Generally, you can consider anything larger than two units a multifamily property or an apartment building. If you’re fairly conservative and only looking to supplement your retirement income or have a sideline income, you may want to stay with buildings no larger than four to six units.

If you’re looking for larger incomes, and willing to take on associated risks, you’ll consider larger buildings like 12 or even 20+ unit buildings.

Know the Types and Classes of Apartments When Buying an Apartment Complex

Apartment buildings come in a variety of forms. There are converted old houses with multiple units, garden apartments with two stories, and perhaps a dozen or more units in a single building, all the way to multi-story mid-rise and high-rise apartment buildings and apartment complexes containing scores of rental units.

In the U.S., there’s a rating scale with letters ranging from A to D, which attempts to classify the caliber of apartment buildings:

- Class “A” Apartment Building: Newer luxury rentals generally 10 years old or less or substantially renovated if older. The will typically take the form of garden, mid-rise, or high-rise buildings. Class “A” apartment complexes have amenities such as pools, tennis courts, and clubhouses.

- Class “B” Apartment Building: Up to 20 years old, and may be dated but are well-constructed and maintained. These complexes may or may not have amenities, but they do, the facilities are more dated than those found in Class “A” apartment properties.

- Class “C” Apartment Building: Up to three decades old, with limited or no amenities. The properties may have an apparent need for renovation and repair.

- Class “D” Apartment Building: Typically over 30 years old and usually in lower socioeconomic areas, often with subsidized housing. Amenities are not typically present, and buildings will usually have an apparent need for renovation and repair.

Most individual investors purchase class “B” and “C” properties because their cost is conspicuously lower than class “A” properties, yet they don’t demand the repairs and renovation and intensive management that class “D” properties require.

Consider Your Return on Investment When Buying an Apartment Complex

How much a building returns is a function of its size and how much cash you have invested in the property. A smaller building with fewer units isn’t going to have the money-making potential of a larger property, but it won’t require as much cash to purchase and it won’t be as management intensive either.

Larger buildings, with more rental units, can produce more income, but they will require a larger upfront investment. Plus, the larger the number of units, the more you’ll need to consider how complex day-to-day management will be. If you have to hire a property manager or engage the services of a property management firm, it will bring down your cash flow and profits.

3. Locate an Apartment Complex to Buy

There are many ways to locate an apartment complex to buy. You can search yourself, without professional help. Local Real Estate Investment Associations (called REIAs) may be helpful with buying an apartment complex. Or, you can enlist the services of professionals, including real estate agents, commercial real estate agents, and even business brokers.

Some of the ways you can locate an apartment complex to buy are:

Search on Your Own for an Apartment Complex

Searching for properties yourself can be time-consuming, but that doesn’t mean it will be unproductive. One of the greatest advantages of searching for properties not handled by real estate agents is that the seller is not paying commission. That’s potentially 6 percent or 7 percent that you might be able to negotiate off the asking price.

Plus, you may be able to get fairly favorable terms by working directly with the seller. You may even be able to negotiate owner financing with the seller and not have to get an outside loan.

Use a Local Real Estate Investment Association (REIA) to Find an Apartment Complex

If you lean towards searching for an apartment building yourself, consider joining your area’s local real estate club. These are typically called Real Estate Investor’s Associations (REIAs). These groups allow you to network with other investors, some of whom may have apartment buildings for sale, or know of someone who does.

Engage a Real Estate Agent

There’s no discounting the fact that the real estate industry provides access to the largest body of properties for sale—and that covers buying apartment buildings. Every real estate agent has access to one or more Multiple Listing Services (MLS) that list all the properties for sale by every agency that participates in that MLS. Multiple-unit properties and apartment buildings will be in that database of properties for sale.

The downside to working with an agent is that a commission will be involved in the sale. Typically, as a buyer, this isn’t coming out of your pocket; it comes out of the seller’s proceeds as one of their closing costs. However, the 3 percent to 10 percent commission will be factored in the price, so it effectively makes the price of the building slightly higher.

Plus, agents know the market and know how to determine values, so buildings will tend to be priced at maximum market value. Be aware: not every agent or even agency is experienced with apartment buildings. So, you’ll want to be sure you are working with someone who is competent in handling multi-unit properties in the size range you are seeking.

Try Using a Commercial Real Estate Agent When Buying an Apartment Complex

Commercial real estate agents specialize in selling and buying apartment complexes. They handle them all the time and probably have better access to listings of apartments for sale than a typical residential real estate office. For example, they may have access to listings with other commercial brokerages that are not part of the typical MLS. Commercial real estate agent commission structures tend to be a bit higher than residential offices, so be prepared to see commissions more in the 7 percent to 10 percent range.

Again, this may not come out of your pocket, but it does influence the asking price of the building. Commercial real estate agencies tend to be a bit more sophisticated than residential firms and will be quick to throw around financial principles you may not yet be familiar with. Don’t be timid; let them know you are a beginner and enlist their assistance in clarifying things you don’t understand. Plus, they regularly work with creative purchase ideas (like owner financing) which residential agents may shy away from.

Consider Using a Business Broker

Business brokers sell businesses, but their offerings include mixed-use buildings (commercial buildings also containing residential units), apartment buildings, and even entire apartment complexes. They can be a great source of potential deals.

Similar to commercial real estate agents, business brokerages are fairly sophisticated offices.

That might mean that they know how to craft and present a creative office. But, it also means they’re accustomed to talking in business finance terms even if you’re not. Don’t be afraid to ask them to clarify what you may not yet understand. In time, you will; until then, don’t be put off by their lingo.

4. Evaluate the Potential Apartment Complex and Neighborhood

When you’re buying an apartment complex and evaluating potential purchases, be sure to assess the location, consider the number and sizes of the units, note the property’s amenities, and pay attention to construction details. This is important to make sure you are aware of any potential issues and can address them proactively.

Then, do two assessments of the finances. Begin by doing a ballpark examination of the basic numbers to see if they indicate it’s even worthy of consideration. If the ballpark examination points to a candidate property, then do a full evaluation of the building’s financials. Again, the importance of this step is to make sure you can address any potential issues early.

More details about evaluating the apartment complex and neighborhood are:

Assess the Location of the Apartment Complex

As with any real estate investment, you want to purchase an apartment building in an area that is desirable. Steer clear of blighted neighborhoods no matter how enticing a cheap purchase may seem. While some investors make class “D” purchases in tough neighborhoods work, there are plenty of good investments elsewhere.

Better located properties provide a stronger base of tenants, better tenants who will take better care of your property, higher rents, and a greater chance of appreciation for the building.

Consider the Number & Size of Units in the Apartment Complex

As mentioned earlier, if you are considering buying apartment buildings, you’ll want to consider how many units each property has. But you’ll also want to consider the size of those units, in terms of square footage, number of bedrooms, baths, and so forth.

Studio or efficiency units can be difficult to rent outside of college campuses and high population areas. One-bedroom units are easier to rent than studios, but your best bet is two-bedroom units and larger. A couple, particularly with a child, will want that second bedroom. Even a single person may want a second bedroom for guests or as a home office. So, it opens up a larger market of potential renters than a one-bedroom does.

Note the Apartment Complex’s Amenities

Amenities help drive interest in your property. These can include everything from washers and dryers in the units to covered parking or garages, and even swimming pools, spas and gyms. There more amenities the property has, typically the more desirable it will be to tenants.

Pay Attention to Construction Details When Buying an Apartment Complex

The five most common problem areas of apartment building construction are:

1. Flat Roof

Flat roofs tend to breed all kinds of problems, particularly related to leaks. However, it’s somewhat hard to avoid them because so many older apartment buildings have flat roofs. Just be aware they can be problematic.

2. All Frame vs. Brick

If a building is all frame, it’s prone to exterior paint and rot issues. That means the more exterior wood, the more exterior maintenance you’ll have to pay for. It also causes a more expensive insurance rating for fire.

3. Old Plumbing

If the building is more than about three decades old and the plumbing has never been replaced, be prepared for a constant stream of plumbing repairs. Old pipe has probably already started to deteriorate. More important, you can have issues with lead in the connections, meaning even costlier repairs to remove it.

4. Shared Utilities

Older apartments often have shared systems such as common water or common electricity. That means the landlord pays that utility and either absorbs it in the rent or tries to prorate it among tenants. Experts agree this tends to be problematic. For example, since tenants feel they aren’t paying for heat, it’s not uncommon for some to raise the thermostat to 80 degrees Fahrenheit in winter, then open a window.

5. Asbestos and Lead Paint

Old buildings often contain asbestos in the insulation, older HVAC systems, and exterior siding. Additionally, the interior may be painted with lead-based paint. Depending on where you live, you may have to mitigate those issues, and it can be costly. In fact, one of the reasons why the owner may be selling is because they are faced with lead or asbestos abatement and can’t afford it. It’s important to have a building inspector look for those materials and check with your city and state to find out what remedies are required if they are present in the building.

Examine the Basic Numbers Before Buying an Apartment Complex

There are several basic numbers you can eyeball on the apartment complex as you are evaluating it. These will provide a preliminary look at the property’s potential before you make a more thorough examination of the property’s financials. These include the apartment complex rent roll, occupancy rate, and cost per unit.

More details about the numbers you should examine before buying an apartment complex are:

Rent Roll of the Apartment Complex

Get the current rental amounts for every unit. Total those and multiply by 12 to get a ballpark idea of the gross annual rent. This is called the rent roll. A tool used by investors, based on the rent roll to compare apartment building purchases, is the gross rent multiplier. It compares the value of the building as a function of rents.

Occupancy Rate of the Apartment Complex

Occupancy rate tells you how much of the time the building is occupied. Vacancy rate is the opposite figure; it tells you how much of the time a building is vacant. Ask the seller and the agent about the occupancy or vacancy rate on the building. Check with real estate agents and landlord groups in your area to find out what the typical vacancy rates are. Compare the figures for the building you are considering to local industry averages.

If the rates seem overly good, then you may not be getting honest information from the seller. If they are poor, try to determine why the occupancy rate isn’t better. There may be opportunities—such as making simple enhancements to units—that can both attract tenants and/or keep them longer.

Cost per Unit in an Apartment Complex

This is a simple figure that is calculated by dividing the building’s purchase price by the number of units it contains. It will give you a point by which you can compare it to other apartment buildings you are considering buying, and compare the figure against local average per-unit pricing. This figure can become a good bargaining tool if you want to purchase the building but you feel the cost is too high.

Evaluate the Full Financials Prior to Buying an Apartment Complex

Looking at the basic numbers gives you a snapshot of how the property looks financially. But, before you make any offer, you need to get a complete set of financials for the property for at least the prior year—and preferably several years.

Numbers like gross operating (rental) income, expenses, vacancy rates, and certain ratios are examining the vital signs for a building and will certainly affect your ability to get financing on an apartment complex.

The numbers to help you evaluate an apartment complex include:

Gross Operating Income

Gross operating income is the actual rent collected on the property. It’s what actually comes in the door allowing for vacancy. If you are buying an apartment complex that is not occupied, then you may need to perform a potential rental income (PRI) analysis. A PRI is based on a rental market analysis, according to the leases and terms of comparable properties in the area.

Expenses

Expenses when buying apartment buildings include interest, insurance, advertising, maintenance, property and other taxes (not income taxes), fees, management expenses, and professional services (like legal help).

It’s important to know what the total expense load is for the year, and what the pattern of expenses looks like each month. Some months will have higher expenses than others, and it’s good to be aware of that.

Net Operating Income (NOI)

Net operating income is what remains from collected rent after paying all expenses. It’s a good idea to examine net operating income both annually and as a monthly figure. Net operating income is also known as cash flow. Cash flow can be a positive figure, meaning you made money during the period, or it can be negative, meaning the property cost you money during that period of time.

Here is an example of computing Net Operating Income for a six-unit building, each unit renting for $600 per month:

| Monthly | Annually | |

|---|---|---|

| Potential Rent Roll | $3,600 | $43,200 |

| -Vacancy (10%) | -$360 | -$4,320 |

| =Gross Operating Income | $3,240 | $38,800 |

| -Expenses | $2,160 | $25,920 |

| =Net Operating Income (Cash Flow) | $1,080 | $12,960 |

In this example, the cash flow is positive, throwing off $1,080 in monthly income, or $12,960 per year!

Profit/Loss Statement

The table above is a simplified version of presenting the monthly/annual finances. You should be provided with what is referred to as a Cash Flow Statement, Income Statement, or Profit/Loss Statement. Fundamentally, these are the same thing. What they provide is a complete picture of the financials, particularly by itemizing all the expenses. So, the profit/loss statement allows you to examine each expense category instead of one lump sum like you see above.

Capitalization Rate

The capitalization rate (cap rate) shows the rate of return on the investment. It’s an important figure that allows you to compare one investment scenario against another, or one property against another.

The formula is:

Cap Rate = Net Operating Income/Purchase Price

Let’s use the example from above, and say the building cost $200,000 to purchase.

Cap Rate = $12,960 / $200,000

Cap Rate = 6.48 percent

Is 6.48 percent a good figure? It depends on a couple of things.

First, it depends on comparison with other units in your area and other units you may be considering. If you are looking at two other prospective properties and their cap rates are 11 percent and 12 percent respectively, then the one above isn’t as good a choice. Or, if cap rates in your area average 9 percent to 10 percent, the building above still pales by comparison.

It also matters how you buy the property. In the example above, let’s presume the $25,920 included interest of approximately $7,000 for the year. If you had paid all cash for the building, you would not have incurred the interest cost. So, your expenses would have only been $18,920. As a result, the net operating income would have been higher by $7,000, or $19,960.

So, the cap rate would be $19,960/$200,000, or 9.98 percent.

Due Diligence Items When Buying Apartment Complexes

If you’ve decided to move forward with a purchase, you need to add a few items to your investigation. Some of these are important enough that you should write them as official requests into the contract and make the offer subject to your approval of what you see. That way, the seller has to provide the information—and you can back out of the deal if the details aren’t to your liking.

Determine Why the Owner Is Selling

When buying an apartment complex, try to ascertain why the owners are selling. The situation that the sellers are faced with is an important component for negotiating the deal. For example, if a seller wants to retire and move to the Sunbelt, his/her motivations are very different than if faced with a property needing major repairs.

Of particular concern is trying to unearth something amiss with the property that the seller tried to hide. Undisclosed problems can cost you dearly and you want to try your hardest to uncover issues before they become your issues!

Obtain Copies of Leases for the Apartment Complex

The only real way to know what the rent roll will look like is to get copies of every lease. Those will show you not only the rent amounts, but also the terms of the lease, who is coming up for renewal, whether they’ve been allowed to keep pets, what their security deposits are, and so forth. Plus, after you take ownership, the leases become yours, so you need to be familiar with them.

Request Prior Owner’s Tax Returns for the Apartment Complex

Often, the books for a property, as expressed by the profit/loss statement, will be quite different than what is reported on the owner’s tax return. Request both and investigate any discrepancies. For example, if the seller shows $12,000 in net operating income on the books, but only $9,500 on the tax return, that should send up some warning flags and should be verified.

Conduct Inspections of the Apartment Complex

When you are seriously considering buying an apartment building—and definitely as a contingency in your contract—you want to get a building inspector to evaluate the property. Apartments are complex and often have shared systems, various levels of condition throughout each unit, and potential issues with common areas that tenants never experience or report. You’ll want a detailed inspection report of what needs to be repaired. That report will become a negotiating tool in the purchase.

5. Make an Offer on the Apartment Complex

Making a good offer on a property involves appraising the value of the building and clearly knowing how rents affect the value of an apartment investment. Keep in mind that if you finance the apartment complex with a traditional bank, they’ll order the appraisal for you. In that case, you may find it helpful to perform a rental market analysis.

Get an Appraisal of the Apartment Complex

Appraisals for apartment buildings are different than for residential properties. There are three methods that will be used side-by-side: 1) market value; 2) replacement cost; and 3) income approach.

The three methods that will be used in an apartment complex appraisal are:

Market Value Approach in an Apartment Complex Appraisal

Appraising market value will look at other, similar properties and their selling prices. If you are considering the purchase of a six-unit building, containing all two-bedroom units, the appraiser will look at similar buildings and what they sold for over the prior year. Market value per-unit is considered in this approach.

Replacement Cost Approach in an Apartment Complex Appraisal

Replacement cost examines the amount it would cost, on a per-square-footage basis, to build a similar building. If you are looking at a four-unit building of 4,000 square feet, and construction costs in your area run $100 per square foot, then the replacement cost will be valued at $400,000.

Income Approach in an Apartment Complex Appraisal

The income approach uses the net operating income and local capitalization rates to determine the value of the investment. To accomplish this, take the net operating income and divide it by the cap rate.

Value = Net Operating Income/Cap Rate

For example, if the net operating income of the building is $46,000 and the cap rate in your area is 10 percent, then:

Value = $46,000/10% = $460,000

Rent Affects the Apartment Building’s Value

Because the income approach is a common tool in appraising apartments, it’s important to understand that if you can raise the rents, you can increase the value of the building.

Let’s say you purchased the above building, and realize the rents are below market. Let’s also say that you own the building for two years, and in that time are able to raise the rents by 20 percent.

For the sake of simplicity, let’s just carry that 20 percent increase to the net operating income, making it $55,200. Using the income approach, the building’s value would then be:

Value = $55,200/10% = $552,000.

You’ve been able to increase the value of the building over $90,000 in two years just by increasing the rents!

6. Finance the Purchase of an Apartment Complex

When buying an apartment complex, successful funding requires understanding the types of financing for apartments, recourse versus non-recourse loans, and lender required reserves. Also, because it affects net operating income, how lenders look at occupancy as part of the loan approval process is also important.

The areas you need to consider when you finance the purchase of an apartment complex are:

Types of Financing for Apartments

Financing for apartments is fundamentally different than with residential purchases. Commercial lending, as opposed to residential lending, is what you will likely use, with conventional loans, seller financing, or private loans your typical options.

Commercial as Opposed to Residential Lending

Apartment buildings will often be financed with commercial as opposed to residential loans. While residential loans may be an option for two- to four-unit buildings, particularly if you are going to live in one of the units, you should familiarize yourself with commercial loans.

To see how much commercial financing you qualify for, check out CoreVest. They provide short-term commercial loans and long-term commercial loans both with competitive rates and terms. Get pre-qualified in a few minutes online.

Conventional Loans

Unless the multi-unit building is four units or less and you plan on living in one of the units, government loans such as Federal Housing (FHA) and Veterans Administration (VA) loans are not available. The vast majority of apartment financing comes in the form of commercial loans from banks and financial institutions.

Private Loans & Seller Financing

The exception to the conventional apartment lending landscape is private financing. The most common is owner financing, in which the seller will allow you to make periodic payments after supplying a decent down payment. Sellers of commercial or investment property like apartments are usually more willing to offer seller financing than homeowners because it’s strictly a business proposition—and the interest they earn means a greater return on their investment.

Because of the potential to earn a healthy interest rate, you might also find private parties willing to lend money on good apartment deals. Instead of you going to a bank, these parties will provide the purchase money and you’ll make payments to them.

Recourse vs. Non-Recourse Loans

With a recourse loan, the lender can pursue financial remedies beyond the building itself should you default on the payments. With a non-recourse loan, the lender can only go after the building itself. Non-recourse loans are the obvious choice, but harder to get.

This brings up an important point about not buying an apartment complex in your personal name. Because of the complexities and risks inherent in apartment ownership—not the least of which is putting your personal finances at risk—you should only buy an apartment complex in the name of a business entity

Your accountant and attorney will help advise you about whether a limited liability company (LLC) or corporation is a better choice, but purchase apartment investments through your entity, not personally as a sole proprietor.

Lender Required Reserves for Buying an Apartment Complex

Lenders will typically require you to maintain one or both of two common types of reserves. The first is interest reserves, which will help ensure you can meet the periodic payments. The other is cash reserves to ensure you can meet operating expenses, insurance, taxes, and repairs.

Combined, reserves may total as much as six months of payments, so be prepared for a fairly big chunk when financing your apartment building purchase.

Key Items Considered by Lenders During the Loan Approval Process

Because net operating income is so important for apartment real estate investing, lenders will look favorably on properties with good market potential, high occupancy rates, and long-term tenants. This is another argument in favor of buying good-grade properties in good areas. Remember: income affects value.

7. Close on the Purchase of the Apartment Complex

Three things to consider when closing on an apartment investment include: 1) selecting an escrow agent or title company experienced with apartments; 2) closing on a financially advantageous day of the month; and 3) having security deposits properly transferred to you.

Select an Escrow Agent or Title Company Experienced with Apartments

As with any kind of real property purchase, you need to select an escrow agent or title company which will help you close the transaction. In some states, attorneys handle real estate closings. In other states, title or escrow companies are used. Whichever is the case in your state, make sure the company has experience with apartment investments and always get title insurance to protect your ownership.

Close on the Apartment Complex on a Financially Advantageous Day of the Month

Rents are paid in advance. Mortgage payments are made in arrears. So closing right after rents are collected provides almost a full month of cushion before your next mortgage payment is due. This is tactic that experienced investors use to pad the purchase a rental property.

Ensure Apartment Complex Security Deposits Are Properly Transferred to You

When you close on the property, any security deposits become your responsibility. Most states require landlords to keep the security deposits in a separate trust account. Even if your state doesn’t require this, don’t make the mistake of thinking that possession of several security deposits is a cash windfall.

That money is technically the tenants until such as time as it may be required for damage or unpaid rent—it’s not yours to spend. So make sure security deposits are properly designated at closing, and get them into a bank account separate from the general one used for the property.

How to Buy an Apartment Complex Frequently Asked Questions (FAQ)

Below, we’re going to answer some of the most frequently asked questions on how to buy an apartment complex. If you have additional questions or would like to comment on the subject, visit the Fit Small Business forum.

Some of the most frequently asked questions about how to buy an apartment complex are:

How Much Money Can You Make if You Buy an Apartment Complex?

Buying an apartment complex can be lucrative if you find a good deal, the property has positive cash flow, and the ROI is high. However, there can be a lot of expenses (e.g., property management fees, rental property insurance, property taxes). These factors affect how much money you make after you buy an apartment complex.

How Do You Buy an Apartment Complex with No Money Down?

Typically, you’ll need at least 10 percent down to buy an apartment complex. However, while rare, there are ways to buy an apartment complex with no money down. This can be done if you wholesale the property, partner with an investor, or find a hard money lender who will finance 100 percent of the loan.

Are There Any Tax Benefits of Buying an Apartment Complex?

There are typically rental property tax benefits involved with an apartment building. Some of these tax benefits include writing off mortgage interest and expenses and repairs and depreciating the building.

Bottom Line

Learning how to buy an apartment complex can generally be explained in seven steps. It’s typically best for more experienced investors. First, you decide if buying an apartment complex is right for you, and then you choose a type of building to purchase based on research and evaluation of the property. Then you typically need to find an apartment building loan.

If you’re wondering where to get an apartment building loan, we have plenty of lenders that can help you. They will typically fund up to 90 percent of the cost on short-term loans and have several other programs for five- to 30-year loan terms. They offer competitive rates and we make sure to shop them for you.